Restaurant Brands International

An Ackman Restaurant Bet

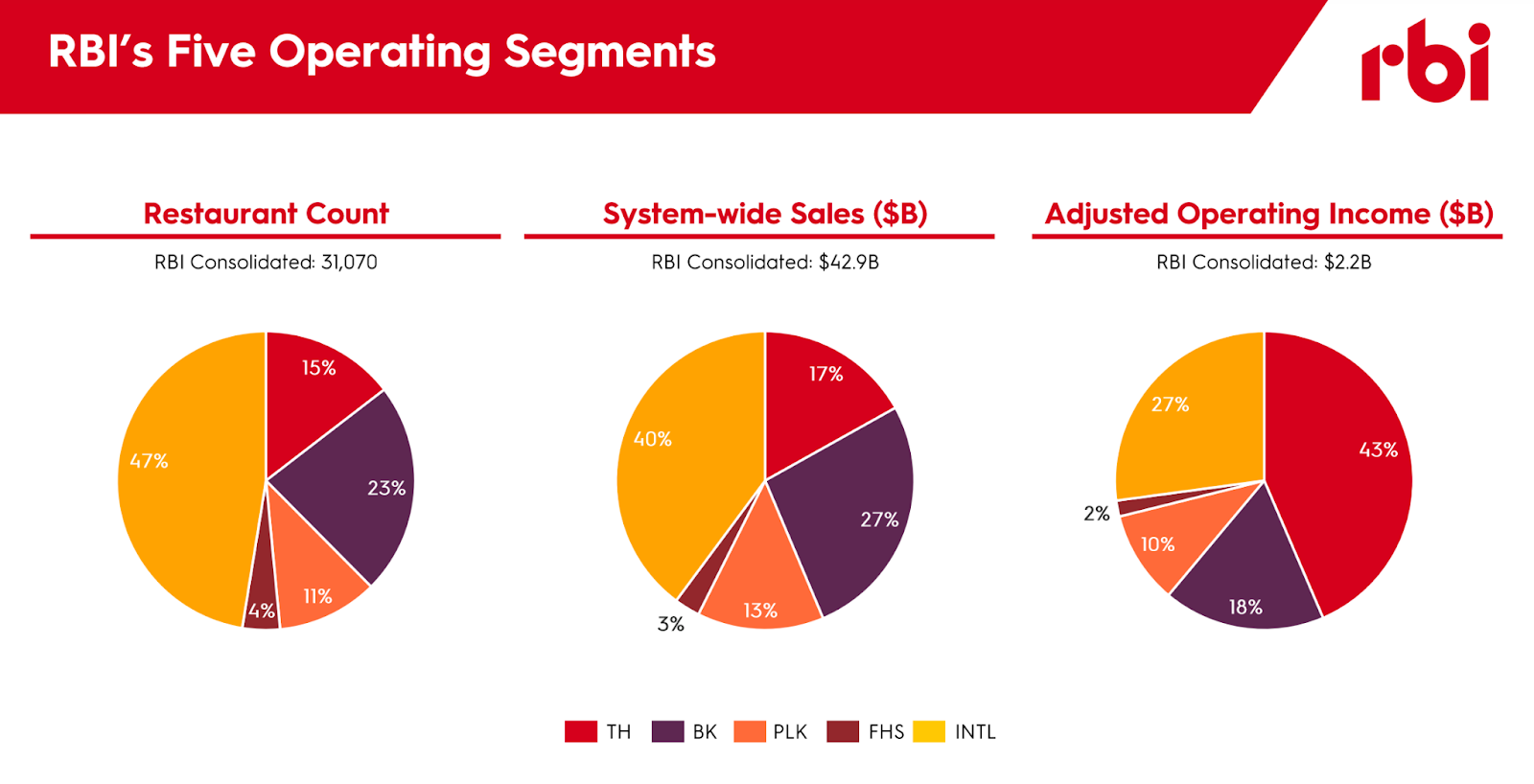

Restaurant Brands International (RBI), formed in 2014, is one of the largest restaurant companies in the world, with four iconic brands: Tim Hortons, Burger King, Popeyes, and Firehouse Subs. The company also recently separated their international segment, which is abbreviated INTL below.

The company operates a restaurant franchise model where franchisees pay a percent of their monthly sales to RBI. Bill Ackman described the company’s business model as “a high-quality, capital-light, growing annuity that generates high-margin brand royalty fees.”

RBI does not operate most of their restaurants; instead, their job is to maintain the quality of the brands and keep their franchisees happy. RBI launches ad campaigns and incentivize franchise remodels to keep the brand fresh. They also look for ways to increase franchisees profitability through things like simplifying the kitchen or reducing store foot prints.

With the recent appointment of J. Patrick Doyle to executive chairman and RBI accounting for 10% of Ackman’s portfolio, I thought the company deserved a look. But first, a quick look at the past.

Howard Johnson’s and The Franchise Restaurant Model

Howard Johnson’s was the first dominant franchise restaurant company in the US, so I thought it would be a good idea to look at their story. Founded in 1925 by Howard Johnson (crazy, I know), the company became the largest restaurant in America during the 50s and 60s with over a thousand locations and its famous ice cream. Howard Johnson is also credited with being the first to apply the franchise model to restaurants.

I will be skipping over the early history of the company as it is not super important for what I am trying to prove here, but if you want to learn more, this source is good: American Business History.

Anyway, by the mid-1960s, Howard Johnson’s became the largest restaurant company in America, and in 1975 they operated 649 company-owned locations and 280 franchised locations (as well as a lot of motor lodges, but again, not important for the story). By 1979, the company had over 1000 locations, but things were not as good as they appeared.

The then CEO, Bud Johnson (the son of Howard Johnson), began exploring ways to reduce operating costs in the face of competition from the likes of McDonald's and Burger King. Unfortunately, the quality of Howard Johnson’s food began to rapidly deteriorate. Furthermore, the company's restaurant locations and brand were becoming antiquated. With decreasing or inconsistent food quality and a failing brand, Bud Johnson sold the company to the Imperial Tobacco Company. After changing hands a few times, the restaurants were no more with the last Howard Johnson’s finally closing in 2022.

Consumers want to eat in clean and relatively upscale locations. It is imperative that restaurant companies update their locations to keep them that way. The food also has to be good, or at least good enough for the price, and consistently so. In retail, and especially in restaurants, you have to win over the customer each visit. According to one study, 51% of people will not return to a restaurant after just one negative experience.

Despite these two seemingly simple ideas, it seems restaurant operators run into issues often. Domino’s Pizza was known for serving terrible pizza before Patrick Doyle; Burger King in the US has a lot of antiquated locations; the same happened to Tim Hortons in Canada, and the list could go on for a while. So what's the secret sauce?

J. Patrick Doyle, one of the all-time great restaurant executives, and Cheryl Bachelder (I think an extremely underrated restaurant executive) both think it's franchise profitability. After joining Restaurant Brands, Doyle put it very simply:

“I have always believed that in a franchise business model, the cash-on-cash returns of the franchisees are the single most important indicator of future success for the brands.”

- J. Patrick Doyle

The more profitable a location is, the more money the franchisee has to invest in the restaurant and upgrade it to keep it modern. This then drives higher volumes, leading to more profits and repeat. From Bachelder, franchisees are also more likely to enforce rules and initiatives from corporate if the franchisees think that corporate is acting in their interest or trying to boost their bottom line. You may be thinking, Well, this doesn’t solve the food issue, but it does. Corporate is the one coming up with the recipes for the food, and if their goal is to make their franchisees as profitable as possible, then they need to make good food.

Another way of looking at it would be that for a franchise company, the customer is not the consumer of the product; it's the franchisee. For a non-franchised retail company, squeezing customers does not get you very far. It is the same for franchised companies and their franchisees. And for an investment perspective, I’ll leave it to Ackman.

“One of the reasons why we like restaurant companies, and we've been a big beneficiary of some very successful investments in restaurants over time is once you get the model right and the economics of the box are attractive and you built a real brand, as long as management maintains focus and consistency and you mitigate the traditional risks of that business, it's sort of a compounding exercise, the opening of stores, the progression of sales over time.”

- Bill Ackman

Burger King

Burger King, or as it was known at the time, Insta-Burger King, was founded in 1953 after the founders visited the original McDonald's and decided the market was big enough for a competitor. Initially reliant on the “Insta-Broiler” to quickly cook up burgers, Burger King switched to a flame broiler after two Cornell students acquired a franchise location in 1954. The students, James McLamore and David Edgerton, then acquired the rest of the company in 1959 after it had gone through some financial trouble. McLamore and Edgerton then changed the name of the company to just “Burger King” and added the Whopper to the menu that same year.

Eight years later the duo sold the company to the Pillsbury Company. It seems almost the entire history of Burger King involves a company trying to turn it around, as Pillsbury tried several turnaround efforts throughout the next decades. Pillsbury launched Operation Phoenix (awesome name), which brought in the McDonald's executive, Donald N. Smith, who attempted to restructure the business but left after three years.

The next guy to step up to the plate was Norman E. Brinker, founder of Brinker International. Brinker launched an ad campaign that attacked McDonald's and caused the Burger Wars (I wonder if we will see something like this again). This campaign proved successful, but after Brinker left the company, Burger King lost its luster, and the company returned to its decline.

Burger King was just passed around between different companies and brands, even being a part of Diageo’s portfolio at one point, until the company was acquired by 3G in 2010. Then in 2012, with the help of Bill Ackman’s SPAC, Justice Holdings, Burger King went public again. Finally, in 2014, after a merger with Tim Hortons, Burger King became Restaurant Brands International. From there an unhappy union was born.

Burger King in North America seems to have been, and continues to be, the company’s problem child. Reading the Pershing Square letters from 2014 to 2023 is just “X should help turnaround” or “Burger King will close the gap to McDonald's this year, guys!” every year. It's hard to say how Burger King in North America has performed since it's been part of Restaurant Brands since their international performance has been so much better, but with Burger King North America's restaurant count sitting at 7,144 at the end of 2023 compared to 7,406 in 2014, things haven’t been spectacular.

Broadly speaking, Burger King seemed to just flounder around, having some success in 2018 and 2019, but with the unveiling of their “Reclaim the Flame” initiative in 2022, things have begun to change. Their two-part plan, which called for a $150 million investment in advertising and a $250 million investment in remodeling and developing technology, looked to bring life back into the segment. By H1 2023, same-store sales had increased 11% relative to pre-COVID levels. Through 2023 and into 2024, Burger King actually outperformed some of its competitors like McDonald's in terms of same-store sales growth. The company remains on track to get 85-90% of its locations to what it calls a “modern image” (basically recently remodeled) by 2028.

With the help of J. Patrick Doyle, RBI has also been able to increase franchisee profitability for Burger King significantly from $140,000 in 2022 to $205,000 in 2023. It seems much of the low-hanging fruit has been picked already, as the company is now aiming for $230,000 of EBITDA by 2026 and a long-term target of $300,000. To help them get even faster, RBI had to acquire a major Burger King franchisor.

Carrols Restaurant Group is the largest Burger King franchise in the United States, accounting for 15% of all Burger King units in the country. Restaurant Brands acquired Carrols in January 2024 for $1 billion at 6.6x EV/EBITDA with a plan of using Carrols’ operating cash flow to update their locations and then refranchise locations once updated.

Of Carrols ~1,000 locations, only 400 or so are “modern imagine,” meaning that they have been updated fairly recently. Using the estimated $500 million of operating cash flow that will come out of Carrols within the next five years, Restaurant Brands plans to remodel the remaining 600 restaurants.

This acquisition, with the goal of refranchising, is pretty clever and will depress earnings in the short term while they reinvest in the business. I think it also shows that management is fully behind their turnaround plans. The remodeling will provide “mid-teens uplifts, net of control, and even better improvements in franchisee profitability,” so this seems like a win.

Burger King North America Future

This is definitely the most disappointing segment that RBI has and I don’t see it getting significantly better for them in the future. There won’t be any unit growth, so all the growth will come from same store sales and operating leverage. The remodeling uplift is definitely a nice tailwind for the company, but after the boost to same store sales, growth will probably normalize to low single digits as there isn’t much room for operating leverage.

Tim Hortons Background and Acquisition

Tim Hortons, the dominant coffee and breakfast QSR in Canada, was started by an NHL player (how Canadian) in 1964. The Toronto Maple Leafs player, Miles “Tim” Horton, opened Tim Horton Donut Shop after an earlier failed hamburger shop. I’m not exactly sure how he expected to find the time to run the donut shop while also playing 70 games a season for the Maple Leafs (and winning the Stanley Cup in 1964 and 1967), but Horton soon met Ron Joyce, who took over operations in 1965. With Joyce’s help, Tim Hortons expanded to 40 locations by 1974.

Unfortunately, that same year, Tim Horton died in a drunk driving accident. Ron Joyce then bought out the Horton Family’s share in the company for just $1 million ($6.4 million today), becoming the sole owner of the company. Joyce greatly increased the speed at which Tim Hortons opened new locations, reaching their 500th location in 1991. In 1995 Wendy’s merged with Tim Hortons until activists pushed Wendy’s to divest the coffee chain in 2006. At that time, Tim Hortons accounted for 23% of all fast food revenue in Canada and 62% of the entire Canadian coffee market.

By 2013, Tim Hortons became the largest QSR in Canada by system-wide sales, with 3,588 locations in the US and Canada. Tim Hortons is so dominant that, at the time, they commanded 42% of the total QSR traffic in Canada, generating $765 million of EBITDA in 2013. They had grown units at 5.5% annually from 2009 to 2013 with 3.1% SSS growth over the same period. The market dominance caught the attention of Burger King, who on August 24, 2014, began their campaign to acquire Tim Hortons, but due to a fairly large amount of backlash from Canadian organizations, the acquisition and merger was not completed until December 15, 2014, when Burger King and Tim Hortons began trading as Restaurant Brands International. The final purchase price for Tim Hortons was $11.4 billion, at ~15x 2013 EBITDA (Dunkin was taken private by Inspire for $11.3 billion at 22x EBITDA in 2020).

By cutting overhead costs by 45%, Tim Hortons reported $907 million in EBITDA for 2015. Unfortunately for Restaurant Brands, that's about where the positives end for Tim Horton’s earnings growth. With the Canadian market already heavily saturated and some missteps along the way leading to deterioration in franchisee relations (including a $500 million class action lawsuit by franchisees saying that Tim Hortons mismanaged the brand), EBITDA has only grown at a 3.8% CAGR from 2013-2022.

In 2018 Restaurant Brands brought in a new management team that launched the “Winning Together” operating plan. The plan called for a $546 million investment in Tim Hortons over the next 4 years. Some of this investment went to improving the look and feel of the restaurants, while other investment went into new product launches. All-day breakfasts and kids menus were launched as a result of the program, along with a loyalty program. Management may have gotten a little overly aggressive with the benefits of this loyalty program, though, with customers redeeming benefits at a greater rate than the increase in earnings, causing EBITDA to decline the next year. Although over 20% of Canadians signed up for the program in under a quarter, perhaps the aggressive benefits were the right call.

Axel Schwan was appointed president of Tim Hortons in 2019 to finish the turnaround by increasing the number of drive-throughs, increasing investment in “brewing technology,” and increasing the quality of its food. Around this time, the brand also expanded into more international markets, like China. Then as things started to look promising, COVID came and wiped out any growth and improvements set for 2020 and 2021. Although there are some positives to be said from this turbulent time. By 2021, Tim Hortons’ share in hot brewed coffee reached 72% in Canada, breakfast reached 59%, and baked goods remained at a crazy 70%.

At their 2022 investor day, Tim Hortons outlined their plan to continue improving the food quality and brand image while exploring avenues for growth as well. Tim Hortons further set out to expand the share of online orders and digital guests, as digital guests spend 4x as much on average compared to non-digital guests. Shockingly, the Tim Hortons app is the second most used “e-commerce” app in Canada, behind only Amazon, and their loyalty program is the third largest in the country. Most importantly, Tim Hortons planned to expand its share in the Canadian cold beverage market and launch more foods for the afternoon. J. Patrick Doyle described this as sort of like McDonald's in reverse.

“When I was young, McDonald's was a hamburger business, and they were crazy to think that they could build a breakfast business. You're a hamburger business, right? They've built one of the best breakfast businesses on the planet. Tim's is exactly the opposite except with a stronger brand with greater penetration, which is something that started as a breakfast business that can be expanded into lunch and into dinner, and that's happening now and it's happening with great success”

- J. Patrick Doyle

Judging from the growth in same store sales from 2021-2024 years averaging high single digits, I think these programs have been a success. More recently, this growth has been almost entirely traffic driven and inspite of the overall industry in Canada. Now with over 4,500 locations in North America generating $284 million of EBITDA in the most recent quarter, Tim Hortons is more dominant than ever.

Tim Hortons North America Future

The future of Tim Hortons in North America will look very similar to the last year or two with a focus on trying to grow their market share in cold beverages and afternoon items. Management is also trying to get the franchisee profitability to $300k over the longer term.

As far as growth for shareholders, Restaurant Brands is only guiding for 400 more units to be added by 2028, which will contribute a little over 2% growth to Tim Hortons in North America. With same store sales growth through pricing and increased penetration into afternoon items combined with some operating leverage, the company may be able to grow earnings somewhere in the mid single digits.

Popeyes Background and Acquisition

The idea of Popeyes first started with Alvin C. Copeland Sr., who opened the precursor to Popeyes, “Chicken on the Run,” in 1972. The standard fried chicken served did little to excite customers and closed after just a few months. But then, just four days later, the restaurant reopened as “Popeyes Mighty Good Chicken” after Copeland had revamped his chicken recipe, adding cajun spices and more of a kick. (Apparently Copeland was quite the perfectionist as well, staying up all night to make his mashed potatoes, for example.)

Copeland changed the name of the company once again to “Popeyes Famous Fried Chicken” in 1975. A year later, the first franchised location opened. While the menu “included clams and livers and gizzards,” their famous buttermilk biscuits were introduced in 1983.

Popeyes grew rapidly to over 500 locations in the US and Canada by 1985, but the growth did not seem to be enough for Copeland, who in 1989 acquired Church’s Chicken for $392 million. Just two years later, Copeland Enterprises went into bankruptcy. A new parent company, America’s Favorite Chicken (AFC), spawned out of the bankruptcy process where Copeland’s creditors were given a stake in the new company. From then on, things were on the up and up. By 1999 the AFC had surpassed $1 billion in sales, and in 2001 the company went public, but not all good things can last for long, and the company entered a period of limbo. In 2004, AFC divested both Church’s Chicken and Cinnabon, which they acquired in 1998.

From 2001 to 2007, the company went through four different CEOs and, as a result, had little to no strategy and terrible relations with their franchisees. The relationship was so bad that a franchisee described it like, “We’re like abused foster children.” Fortunately, the company finally found the correct person to lead their company, Cheryl A. Bachelder.

Bachelder got to work quickly, and after a meeting with many Popeyes franchisees, Bachelder and her team came up with a model of leadership that made the franchisees the number one priority because after all, “no one has more skin in the game than [the] franchisees.”. The team chose this model in part because Bachelder had found that legislation and instituting rules often did not lead directly to better service. There are a lot of people between the CEO and employee, and if all are not on board, those rules will not consistently make it to the employee working the cash register. With the new franchisee-first model, Bachedler and her team would hopefully win over the franchisee, who would then be more willing to enforce rules sent from the executive suite.

The company began tracking restaurant-level profitability and made that their most important metric because that was what was most important to the franchisees. (This effort resulted in franchisee EBITDA doubling from 2008-2015.) Bachedler then met with 10 large franchisees to present her plan for the new rollout of national advertising, and while the franchisees liked it, they wanted Popeyes to spend an additional $6 million on advertising. Despite hurting earnings in the short term, Bachedler agreed, knowing that in the long term the additional advertising expense would drive more sales.

Bachedler’s focus on serving the franchisee and acting in their best interest, even if it temporarily hurt the stock price of Popeyes, delivered some fantastic returns. Under her leadership, the stock delivered a 20% annualized return, going from ~$15 in November 2007 to $79 when Restaurant Brands acquired them in February 2017. (The company was also renamed for the last time to Popeyes Louisiana Kitchen in 2014.)

It was advertised that Restaurant Brands paid $1.8 billion, or 21x EV/EBITDA, the highest multiple paid for a restaurant acquisition in the US at the time; however, in RBI’s annual report, it states that the company only paid $1.654 billion ($1.3 billion in debt), and according to Popeye’s 10k, they generated $88.7m of EBITDA in 2016. Still 18.6x EBITDA, but maybe not as much of a nosebleed for a brand with 2,688 system restaurants and ample room to grow.

With 3G as the controlling shareholder, costs were bound to be cut. By integrating the back offices and instituting zero-based budgeting, SG&A expenses were cut from $89.5m to $40.2m, and total costs were cut by around $80m. Popeye’s was able to report $106m of EBITDA in 2017 with more than a 1,500 basis point increase in EBITDA margins. Even with the PE-style Machiavellian cost-cutting, the president of Popeyes, Sami Siddiqui, wanted to see what made Popeyes different. He actually worked the line at several locations to understand the company. He saw how the chicken was marinated for 12 hours and how the chicken was only to sit out ready to be served for 30 minutes at most. Through this experience, Siddiqui found avenues to improve the line, like changing the kitchen lay out and leaving some product development to the suppliers.

In 2018 the company then expanded their value offerings, driving customer satisfaction up 10% in around 5 months while signing master franchises to take Popeyes to Brazil and the Philippines. RBI also began installing standardized POS terminals at Popeyes locations and rolled out delivery at 50% of locations within the year. However, their most impressive and famous initiative was not tech-related. It was Popeye's chicken sandwich that was released in 2019, which also started the chicken sandwich wars.

Released nationwide on August 12, 2019, to lines wrapping around the block with over 100% increases in traffic at locations. In less than two weeks, restaurants around the country were completely sold out, and on August 27th, Popeyes officially announced they were sold out across the entire country. A man was even killed after someone was accused of cutting in line to get the chicken sandwich at a Popeyes in Maryland. This naturally led to crazy sales growth for the company, with global same-store sales growing 12.1% in 2019 and 13.8% the year after.

With the help of the chicken sandwich and RBI’s ownership, Popeyes has outperformed in most metrics relative to Popeyes as a standalone company. Popeyes’ total restaurant count at the end of 2023 was 4,571 locations around the globe vs 2,688 at the end of 2016. EBITDA has grown at 18.2% annually from when it was acquired to 2022; system-wide sales have grown at 11.2%, and unit growth is at 7.3% over the same time period. To compare, from the end of 2009 to the end of 2016, Popeyes, as an independent company, grew EBITDA by 11.7% annually, system-wide sales by 8.3% annually, and total units by 4.75% annually.

I think this acquisition, despite the optically high multiple, can be put down as a success. If Popeyes were to be sold at 17x EV/EBITDA in 2022, that would be something like a 16% annualized return without accounting for the interest payments.

However, I did say Popeyes has outperformed in most metrics, not all. On the Q3 2017 call, management stated that they were confident they would be able to increase owner profitability, which, as we saw from Bachedler, is an important metric. Unfortunately, domestic franchise profitability has actually declined by over $100k, despite AUV increasing from $1.4m to over $1.8m. In 2016, Popeyes said their domestic franchise profitability was $333k, but in 2023 it was just $245k.

Popeyes Future

J. Patrick Doyle’s main priority for Popeyes seems to be getting them back to their Bachelder levels of franchisee profitability. Restaurant Brands is targeting $300,000 in EBITDA by 2025, and it will be interesting to see if they hit this with their earnings soon. This will likely come through simplifying the kitchens and units, growing their digital mix to greater than 25%, and increasing convenience. For example, after COVID, 60% of orders were through the drive through, so management has cut the average number of seats at franchise locations from 72 down to 25-25 seats.

With so many people going through the drive through, the company loses a big chance of getting loyalty members, so they are working on ways to boost loyalty members. They are also increasing convenience with more drive throughs. “Popeyes said last year more than 50 percent of pipeline stores featured double drive-thru designs. In 2022, over 70 percent of openings had at least one drive-thru.”

Management also sees a path for 4,200 locations in North America by 2028 compared to the roughly 3,400 locations they currently have. With low single digit same store sales growth, this segment could fairly easily reach management’s guidance of 8% operating income growth.

Firehouse Subs Background, Acquisition, and Future

Firehouse Subs was founded by brothers and firefighters Chris Sorensen and Robin Sorensen, who, after trying real estate, rock n’ roll, and Christmas tree farming, ultimately found success with subs. Their first location opened in Jacksonville, Florida, on October 10th, 1994. From there the company was able to grow fairly consistently, reaching 500 locations in 2012 and 1000 locations in 2016. Then, for whatever reason, unit growth slowed to almost nothing. The next five years the company only added around 200 locations, and in 2021 it was acquired by RBI for a little over $1 billion for 33x EBITDA (20x adjusted).

At the time of acquisition, the company had $1.15 billion in systemwide sales and a 3.5-year franchise payback period. Interestingly, the company has hardly grown under RBI. Global restaurants stood at 1282 for 2023 vs. 1213 for 2021, but EBITDA has increased by 15%. Management has not discussed Firehouse very much, which is a somewhat worrying sign. With that being said, they have begun discussing it slightly more recently.

In the 2024 company overview presentation, management did say they have an “aspiration” (strange word choice) to add 800 restaurants within the next five years. On the Q4 2023 call, management mentioned that restaurant-level profitability increased 38% from $80,000 to $110,000 in 2023, and the company recently announced a 500-store expansion plan into Brazil over the next 10 years. Management also wants to make Firehouse the first fully digital restaurant concept, which could boost margins, but I’m not entirely convinced. On every presentation, the company also likes to point to the fact that Subway has a crazy amount of locations, but that is just not repeatable. Subway had a first-mover advantage and a low franchise fee compared to the 6% that Firehouse has.

With so many scaled competitors (Subway) or identical competitors (Jersey Mikes), I’m far from convinced this was a good acquisition. With Firehouse only accounting for 2% of operating income, it will take some substantial growth to move the needle for shareholders.

International

The international part of Restaurant Brands International “is the crown jewel of the company, as it is a pure franchise royalty business, with a decades-long opportunity for unit growth.” RBI separated the segment from its other brands to give investors more visibility into their crown jewel, but I was not sure how to implement it into my write-up, so it's just kind of here.

In stark contrast to Burger King in North America, Burger King in the international markets has been killing it for quite some time, thanks to fresher and newer locations compared to competitors. The results are pretty clear; French Burger Kings, for example, have AUVs of close to $4 million. Burger King’s international systemwide sales have grown at an 8% annualized rate since 2017. Interestingly, there is almost a duopoly in the international burger market with McDonald's and Burger King. McDonald's is twice as large as Burger King, but Burger King is six times larger than the next closest competitor.

As for Tim Hortons, international expansion is somewhat of a new journey for the brand. In 2014 there were just 150 locations outside of the US and Canada, but by June 2023, RBI had grown that to 1161. Tim Hortons has had some trouble in China, and with over 130,000 coffee shops in China, I can’t imagine why.

Popeyes was in a similar situation, only growing international units from 540 in 2017 to 603 in 2020, but since COVID they have added close to 400 additional locations. What makes Popeyes more interesting to me than Tim Hortons is that KFC is really the only scaled player in international markets. KFC is 23x larger than Popeyes in terms of units, but when compared to the burger market, there could be substantial room for growth. McDonald's and Burger King have over 36,000 locations internationally, while KFC and Popeyes have 24,000. I honestly don’t see why this gap could not be closed with some nicely done execution.

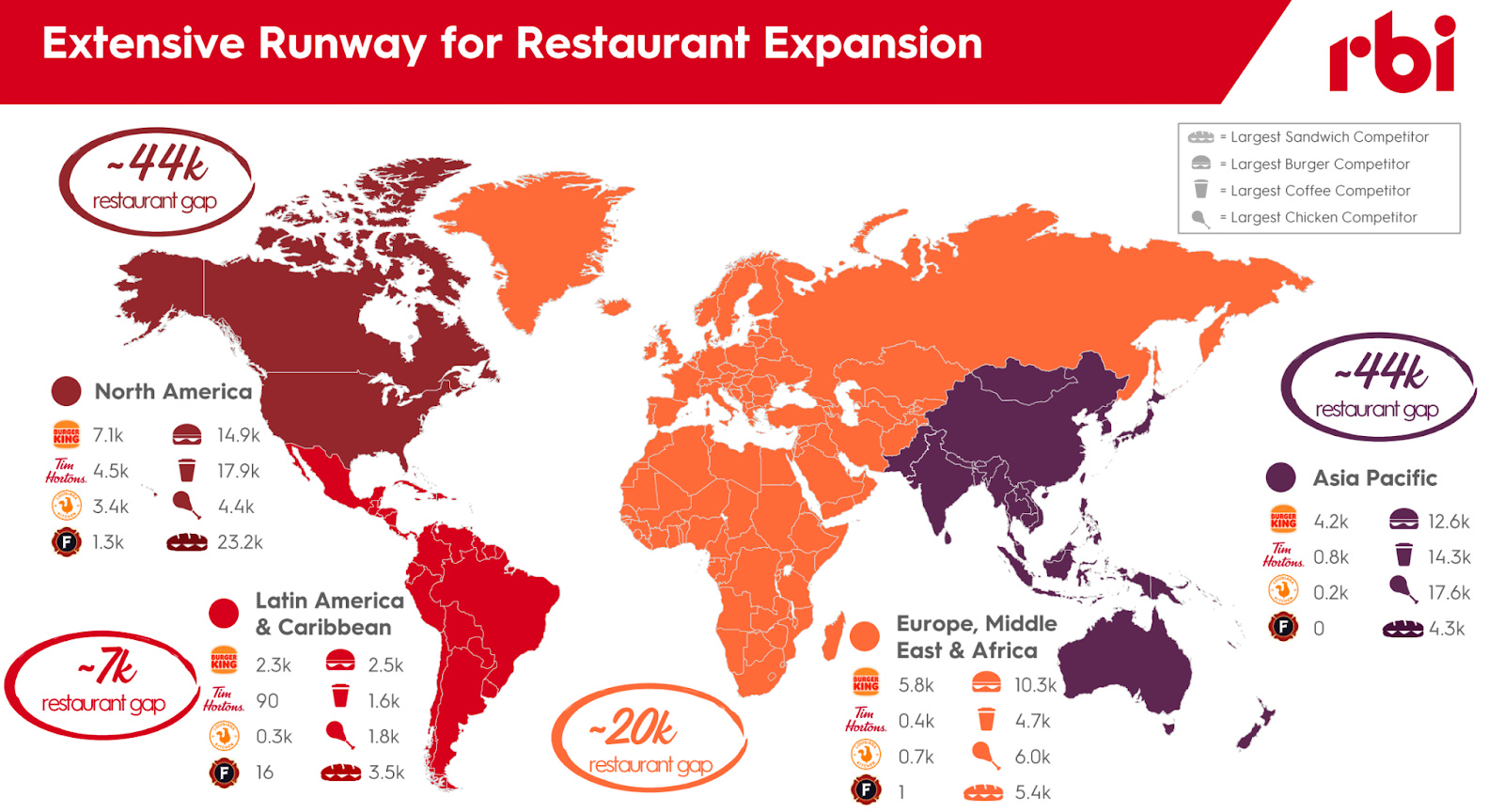

As a whole, the segment has been killing it. Comparable sales have grown on average at 12.8% from 2021-2023, and system-wide sales have grown at 24% over that same period. Management is guiding for 7,000 new restaurants by 2028 for the international segment, which is close to a 50% jump in unit count. Even after those additional units, the company would only have 21,000 units with substantial growth left. Management likes to show this slide whenever they can, and while ambitious with many of these markets already saturated, it does show the opportunity.

Management & Compensation

The star of the management team is undoubtedly the Executive Chairman, J. Patrick Doyle. After he admitted the pizza tasted like cardboard, he became the CEO of Domino’s Pizza in 2010, delivering something like a 2,500% return in eight years. Even after just a few years at RBI, the results are already showing. He has made franchisee profitability the top priority and within a year increased it across the company by something like 30%. The guy has to be a wizard or something, but won’t be here forever. Doyle explained his role at the company in an investor conference.

“I have an enviable opportunity at this point in my career to be an advisor to Josh as he takes on his new role. My own mandate here at RBI is to rapidly accelerate the growth of the company by identifying areas that can deliver outsized results as we lean into them even more.” - Doyle Q4

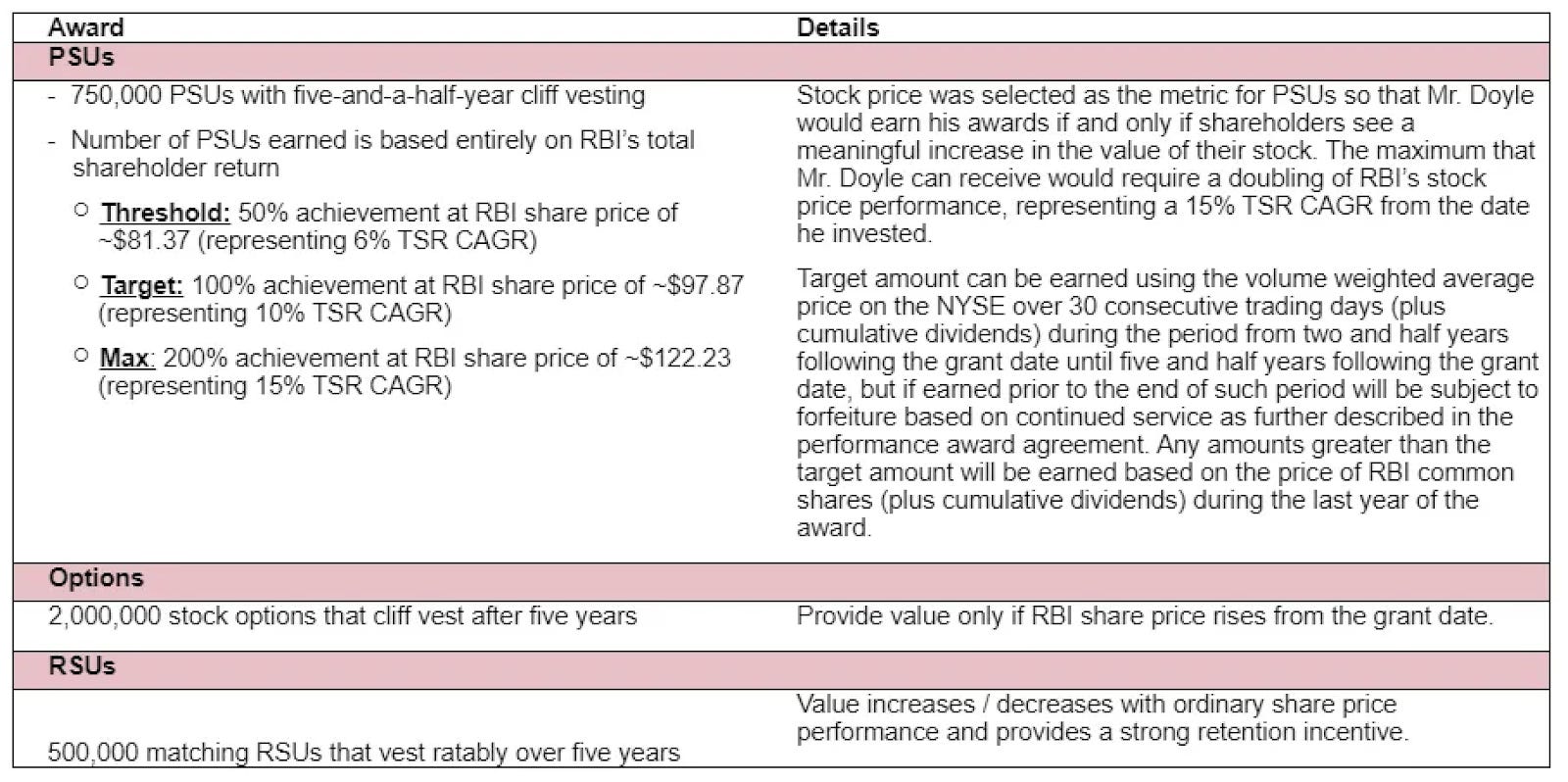

When J. Patrick Doyle joined the board he invested $30 million into the company, but that is nothing compared to his compensation package:

Executives are not in the practice of giving themselves goals that are impossible to hit. With the current share price requiring a 50% gain to hit the target compensation, things look appetizing. My concern is that management does some stupid shit to try and send the stock price up to hit their thresholds though. The amount of shareholder dilution is also a concern that I will touch on later.

Joshua Kobza is the CEO of the company and I do feel somewhat bad that he is entirely overshadowed by Doyle, but at least he is learning from him. Prior to the CEO role he served as CTO and CFO of the company from December 2014. From what I can tell he seems like a competent guy and it certainly helps that he has J. Patrick Doyle advising him. His compensation is the same as Doyle’s, but with only 300,000 PSUs and no options or RSUs.

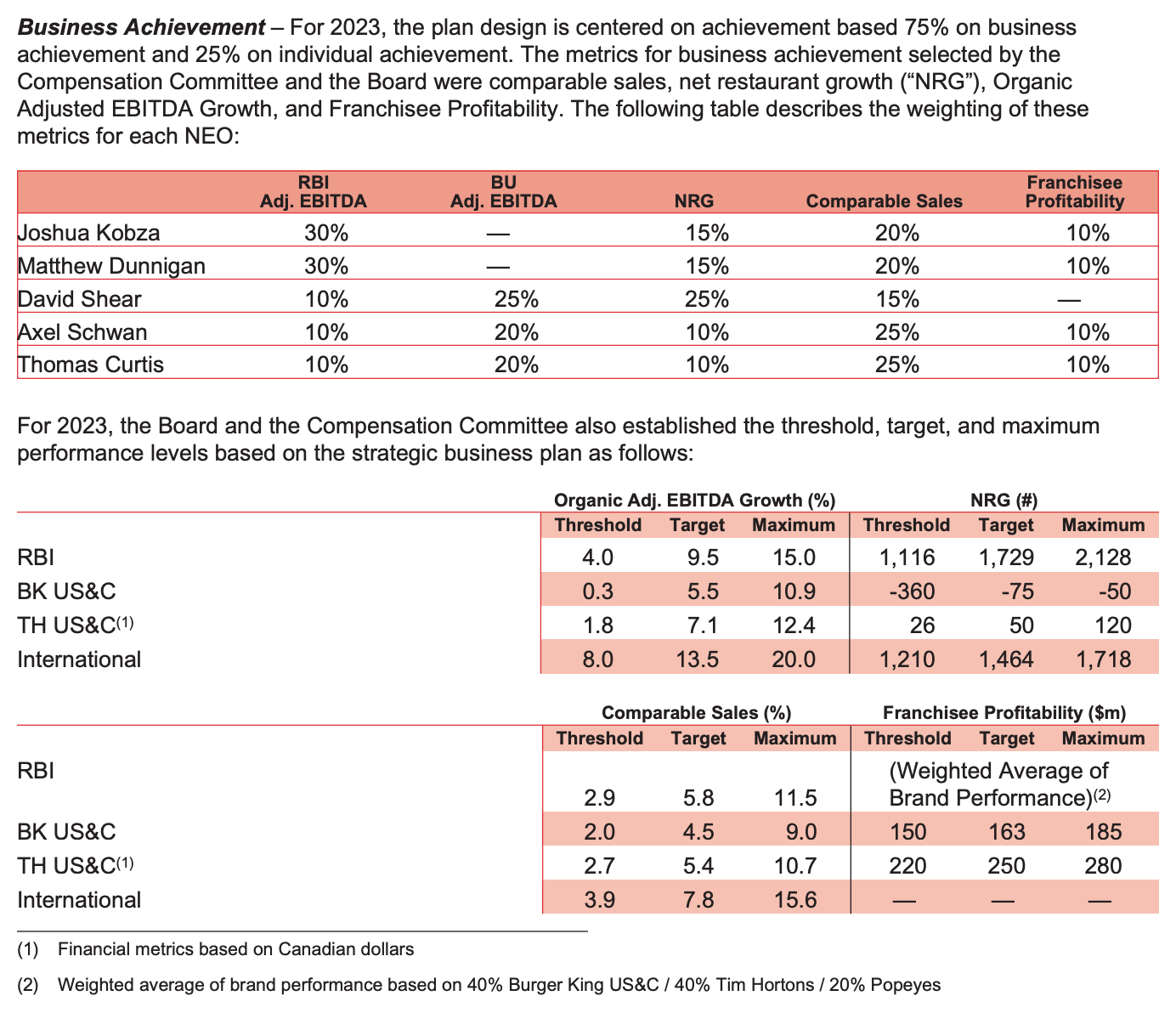

The presidents of each division have compensation packages that are definitely on the better end of what I have seen, but I don’t like the adjusted EBITDA part, I would prefer some type of cash flow metric instead.

Something that is definitely interesting about this package is again the target values. Despite the presentations guiding for 8% operating income growth, the target value for the president's compensation is actually 9.5% EBITDA growth. What's more, look at the international segment with a target of 13.5% and a maximum of 20%. Looking at the franchisee profitability, the company exceeded their target goal for the year, so perhaps these numbers really aren’t that crazy.

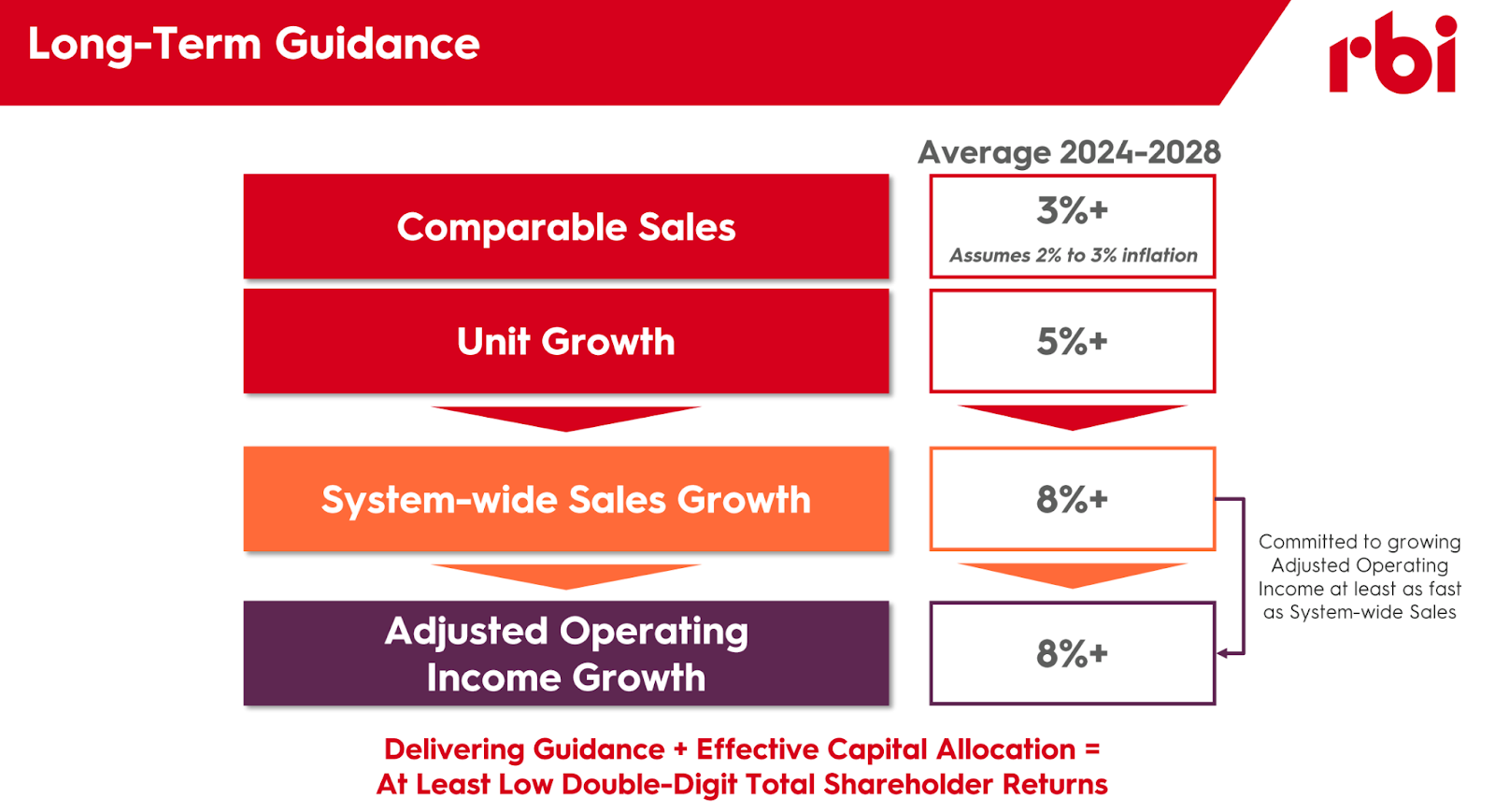

Valuation

Management has laid out their long-term guidance of 8%+ operating income growth.

J. Patrick Doyle; however, thinks this is conservative, saying “I really believe that it is the lowest average annual performance you will see over time with some real upside potential.”

To make things really simple for a second, if we take management's guidance of 8% growth + 3.5% dividend yield + a rerate from 13 to 16x EBITDA in 5 years, forward returns from here are over 15%. That doesn’t account for any operating leverage that is going to undoubtedly come, especially out of the international segment as locations reach maturity. Doyle has also said that their current G&A levels are sufficient to drive future growth. Nor does it account for the excess spending for Burger King or any shares the company may repurchase once their leverage is low enough.

Ackman is obviously quite bullish with Restaurant Brand’s making up around 10% of his portfolio. He described the company’s business model as “a high-quality, capital-light, growing annuity that generates high-margin brand royalty fees,” and in his letters seems to constantly say the company is undervalued, even at 25x earnings.

Taking a look at the Carrols acquisition, there are roughly 1,000 Burger King restaurants, generating ~$1.7 million in restaurant sales. When most of these are refranchised in 2028 and beyond, Restaurant Brands could see an $80 million annual cash flow uplift coming from low single digit SSS growth, the remodeling sales lift, and the 4.5% franchise royalty. These locations will also be sold at market rates, providing an additional several hundred million dollars that could be used for share buybacks as well.

What's more, the “Reclaim the Flame” program is just a temporary investment in the company, and as that program ends there will be more cash that can be returned to shareholders. When combining the “Reclaim the Flame” expenses with the Carrols acquisition, RBI will likely be seeing an $100-150 million increase in earnings in the next few years. It seems that the market is not factoring these in as of late.

Unfortunately it's not all sunshine and roses. While shares outstanding sits at 312 million, diluted shares outstanding is 456 million thanks to the huge compensation packages and Restaurant Brand’s partnership exchangeable units from the Burger King Tim Hortons merger to form RBI. Using shares outstanding would materially overestimate earnings on a per share basis.

Returning to management’s guidance, RBI should produce $3.2 billion in EBITDA by 2028, and with 456 million shares outstanding, EBITDA per share would be $7. At 16x EBITDA, the share price would be around 112 vs. ~60 today. It seems like even the share dilution is factored in at the current price.

Why Hasn’t This Traded Higher?

Something that may have stopped RBI from trading more in line with its competitors is that it has always had some sort of fire to put out, whether that be Burger King in the US or Tim Hortons. With a whole new management team in place that has already got these businesses back on track and should be able to hold them in line, hopefully the market prescribes a higher multiple.

Two other lesser things may be that the majority of the company’s profits come from outside the United States, making it seem like a Canadian or international company rather than American. Also, the high amount of leverage the company operates with most certainly scares some people off. However, given the nature of the business, the leverage is not a huge concern.

Competitors

I’ve made the mistake (and might be making it with a company in my portfolio right now) of investing in companies as if they existed in isolation. To alleviate this, I’ll provide a little information on RBI’s competitors and what they might be looking to do in the future.

McDonalds is looking to aggressively expand their chicken sandwich and other chicken products, which naturally would impact Popeyes. McDonalds is also looking to expand to 50,000 restaurants by 2027. They aren’t just expanding the company either, 44% of capex is going towards reinvestment as well. Like Restaurant Brands, they too are investing in digital and drive thru locations to increase convenience. McDonalds is a great executor and should continue to be into the future.

Yum Brands, the owner of KFC and Taco Bowl, is also looking to accelerate their international expansion. Yum Brands is guiding for 4-5% long term unit growth, which would add around 2,500 locations annually. Interestingly, their growth algorithm is very similar to RBIs and they’re also guiding for high single digit growth in EBITDA. Just like the other guys, Yum is also investing in digital and their loyalty programs. I’m not sure about the Yum Brands management team, but the CEO of Yum China, Joey Wat, is a very smart lady who seems to understand capital allocation well.

RBI’s competitors are great companies, so it will not be a walk in the park for them, but with Restaurant Brand’s exception management, who focus on franchisee profitability, valuable brands, and a cheap valuation, it seems likely that you could do well investing in RBI from here.