Just a quick heads up. This is not nearly as in depth as my two previous write ups. Consider this a company primer rather than an investment thesis. Then again the company and thesis are very simple. I’m waiting for a pullback in valuation before I look into this company again.

Overview

Maritime shipping is the single most important component of global shipping; some estimates suggest that 80% of all goods are transported via maritime shipping. Shipping goods over water is often the only way for goods to cross continents and is by far the cheapest. For context, Fulfilrite found that shipping goods from Shanghai to New Jersey cost them 5x more by plane than by sea. And that is just for pallets. Good luck trying to fly hundreds of tons of coal from somewhere like Baltimore to Mundra, India. The huge cost advantages that the maritime shipping industry possess will continue to be around until well after I die and that’s something I like to see. Unfortunately, being a vessel owner/operator is not nearly as spectacular. The industry goes through massive bouts of over supply that constrain freight rates and forces many companies to operate at heavy losses for years before something changes.

However, what if there was some kind of toll road for the industry? That way, the cyclicality of freight rates would not matter. I had looked at individual port operators, but they are tied too closely to one economic zone and often lumped in with less desirable assets.

I believe Svitzer is that toll road. Svitzer is the largest tugboat operator in the world, with operations in 37 countries and in over 180 ports and terminals. It was spun off from Maersk earlier this year. Initially established as a salvage company, Svitzer has since expanded its operations and now specializes in towage. The company’s fleet of tugboats and emergency response vessels helps facilitate the safe and efficient movement of large ships in and out of harbors, assists with docking, and provides emergency response services. Svitzer plays a crucial role in supporting the global supply chain by ensuring that ports operate smoothly and safely, enhancing the efficiency of commercial shipping logistics. Every 3-4 minutes they complete a tug job around the world.

The Business

Harbor Towage

Representing almost 70% of the company’s revenue, harbor towage is the largest segment at Svitzer. Operating in over 140 ports worldwide, mainly in Europe and Australia, Svitzer completed more than 150,000 tug jobs in 2023 alone.

Svitzer enters two types of contracts: open port contracts and concession/license-based contracts. Open port contracts apply in ports that are open to any tug operator. The agreement is typically between the owner/operator of the vessel and Svitzer, usually lasting 1-3 years. In these contracts, customers are charged per tug job, with annual price adjustments built in. There are few barriers to entry, aside from minimum requirements set by the port. While the initial investment may price out smaller competitors, Svitzer can usually recover nearly all of this investment at the end of the contract.

I find that concession/license contracts are more advantageous than open port contracts. These agreements are between the port operator and Svitzer, granting Svitzer the exclusive right to operate in that port. With contracts lasting between 5 and 10 years, Svitzer gains a high degree of visibility into future earnings. Svitzer also makes contracts with vessel owner/operators under similar terms to those in open ports. Often, the price per tug job is partly regulated by the port, which aims to ensure it remains an attractive destination for ships. While fees might be lower with these contracts, the volume and stability from being the sole tug operator at a port more than compensate.

These contracts have provided Svitzer’s harbor towage segment with impressively stable growth over the past five years, even through economic cycles.

While there can be competition to win new contracts, in some ports that have strange weather conditions, like Southampton's “double high tides”, Svitzer has been the exclusive tug operator for the last 10 years. The risk of switching to a less experienced company is just too great. Furthermore, the fact that revenue growth has outpaced projected market growth suggests Svitzer is winning substantially more contracts than losing. Over the last six years the company has entered 10 new ports and exited 5 (of which were sold rather than lost). While this segment is less predictable than the next segment I will touch on, it still possesses some excellent qualities and a fairly high degree of visibility into earnings that make it attractive.

Terminal Towage

Now this is where the fun begins. Although terminal towage represents only 30% of revenue and 40% of EBITDA, it has some highly attractive qualities—making it my favorite part of the business.

Terminal towage contracts are agreements between the terminal operator, typically an oil and gas company, and Svitzer. Under these contracts, Svitzer provides a set number of tugboats at fixed daily rates, regardless of the volume of activity (even if it's zero). These contracts often require higher upfront costs than harbor towage because tugboats may need to be custom-built to meet contract specifications, which further limits competition. Even better, the average contract length is 10 years, with some contracts extending up to 30 years. Svitzer also benefits from contract price escalators linked to inflation and other increases in operating costs. Importantly, capital is only committed to building the tugboats after the contract has been signed.

To quickly summarize the advantages of these contracts:

Average contract length of 10 years

Fixed daily rates, independent of volume

Price escalators embedded in the contracts

Capital is committed only once the contract is signed

Thanks to these features, Svitzer has 13 billion DKK in secured revenues, with 85% of that set to come after 2025. This segment essentially functions like an equity bond.

Svitzer has a 94% contract renewal rate and a 59% contract win rate (it may actually 76%, but their CMD slide is confusing. I’m not sure if they are counting renewals as wins or if that is separate). This is largely due to Svitzer being able to cut lead times down from when the contract is signed to when they can start operations and their operational history. I could continue talking about how fantastic this segment is, but I think you get the picture.

The Growth Formula

Svitzer’s future growth can be broken down into three key areas that can be easily monitored:

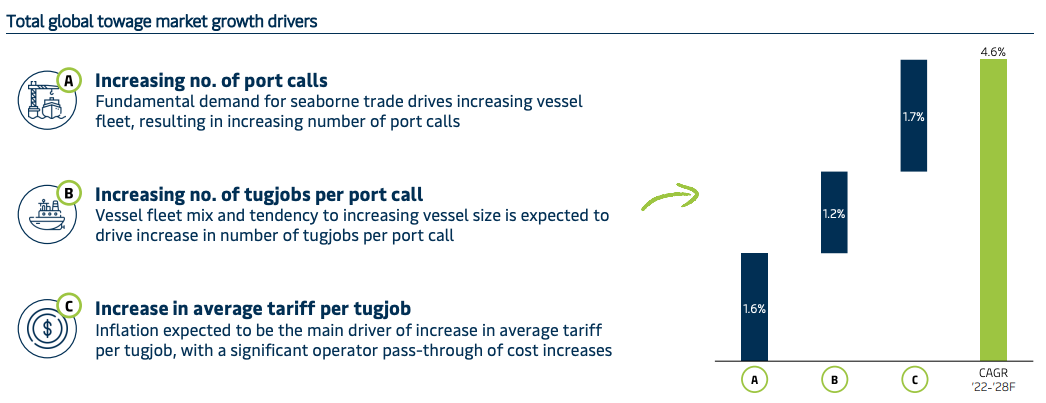

Larger and Larger Ships

Cargo ships and other vessels continue to grow in size, reaching enormous scales. Since 2000, the world’s largest ship has nearly tripled in size. Today, the largest container ships can carry 20,000 TEU. What is a TEU? It stands for "twenty-foot equivalent unit," essentially a standard shipping container. Just two of these containers are larger than my dorm room, and 20,000 TEU is roughly equivalent to the carrying capacity of a 44-mile-long train. As these ships grow larger and heavier, they require more tugboats to maneuver in and out of ports, a promising trend for Svitzer. While exact data on ship size growth is limited, we know ships are getting bigger, and that's a positive tailwind for the company.

More and More Ships

An increase in global ship traffic means more ships will require tugboat assistance when arriving at ports. Svitzer estimates that the number of vessels will grow at a compound annual growth rate (CAGR) of 1.4% from 2022 to 2028. However, a market report from BIMCO in September 2024 states, “Ship supply is expected to grow by an average of 10.3% in 2024 and 6.3% in 2025.” This growth, driven by record-high new ship deliveries, is largely due to disruptions in the Red Sea that have forced ships to reroute around the Cape of Good Hope. Once these disruptions ease, growth will likely return to Svitzer’s estimated 1.4%. From 2011 to 2022, the global container ship fleet grew at about 1% annually, suggesting Svitzer’s estimate is reasonable. As the global fleet expands, Svitzer will perform more tug jobs, another component of its growth formula.

Inflation and Inflation Ships

Ignore the title, I just wanted to keep the pattern going. Svitzer can raise its average tariff through price escalators tied to inflation and other cost pass-throughs. The company projects price increases of 1-3% per year to offset costs. With towing fees representing less than 1% of total voyage costs, customers are unlikely to object to these adjustments.

When combining these three components, the global towage market is expected to grow at a rate of 4.6% over the coming years. Svitzer’s addressable market will likely grow slightly slower, at 4.4%, though this does not account for potential new contract wins.

Competition

The towage competitive landscape is not at all what I expected. It is yet another industry with a few scaled players and then a massive right tail.

The second largest tug operator, Boluda, has completed several acquisitions and even attempted to acquire the fifth largest tug operator, Smit Lamnalco. So although Svitzer is currently the largest tug operator in the world with a 12% market share, it is possible that they get usurped by Boluda some time in the near future if they have not already. This will not be detrimental, but it is maybe something to keep track of.

I’d like to see Svitzer start to acquire some of the smaller competitors in the space. The contractual nature of the business makes the risk much lower than other roll ups and it would juice growth a bit. We will have to wait and see if they do decide to do this or not.

Valuation

From the growth formula just discussed, 4% base growth is probably fair. However as mentioned this does not include new contract wins that Svitzer will undoubtedly be able to get in the future. These wins seem to add 1-2% towards growth, resulting in 5-6% growth for the company.

While the company does break out growth capex, this is still a cash expense and if we are assuming that Svitzer wins contracts in the future it must come from that growth capex. In a terminal value situation then I would take into account growth capex, but since the company is still growing it would be silly to add it back to free cash flow.

With that, Svitzer should generate around 600m DKK this year from management's guidance. Due to the stability and high visibility of the business and 5-6% growth from the company, a 20-25x EV/FCF multiple seems fair (5-6% growth + 4% free cash flow yield = around market returns). Thus with the basic assumptions of 6% growth for the next 5 years and 25x EV/FCF on exit, we would see about a 12.5% return from the current price. The company has committed to paying 40-60% of annual net profit as a dividend so capital will be returned to shareholders.

This is by no means an extensive valuation process, instead I am looking to see if returns are obvious enough to justify a position. At the end of the day, when we are valuing a stock, we are predicting the future, so the more assumptions we make, the more wrong we will most likely be.