Valvoline

For a while now I’ve wanted to try and find the next Autozone: a company that can pretty much grow during any environment while aggressively buying back stock. Autozone has returned +20% annualized for the last 17 years, so you can see why I’ve wanted to find another one.

While Valvoline may not actually be the next Autozone, it does have some very similar characteristics now that they have sold their Global Products segment to Aramco. There are a few other trends that I remembered from looking at Copart that also made me super interested in these preventative-maintenance businesses, so here we go.

History

Dr. John Ellis founded Valvoline, then called the "Continuous Oil Refining Company," in 1866 after synthesizing the first petroleum based lubricant for steam engines. The lubricant name itself was changed to Valvoline in 1868. Throughout the rest of the 19th century, the company became the go to brand for lubricants and became highly recommended by racing car champions. The largest breakthrough occurred when Henry Ford solely recommended Valvoline as the lubricant for his Model-T. In 1949, Valvoline was acquired by Ashland, during that time, Valvoline continued to innovate and produce new lubricants. They made a bunch of iterations on their lubricants and as someone who doesn’t even have a car, I don’t really get it that much. Basically they made better and better lubricants throughout the rest of the 20th century and until today. In mid 2017, Valvoline was spun off from Ashland, but Valvoline actually IPOed in late 2016. Four days ago, August 1st 2022, Valvoline announced the sale of their Global Products business, which synthesizes the lubricants, to Aramco, marking a very significant change in their business.

The Sale of Global Products

My thesis does rest on the idea that the deal will close between Aramco and Valvoline, and while I don’t see any reason for it not to go through, I figured I would touch on a few points. The timing of the sale is interesting with the increased price of oil hurting the margins of Valvoline. I think the sale was both to get rid of a business segment where they could not control prices, while also unlocking shareholder value. The sale price of $2.65b means that Aramco paid 13x fcf or 8x EBITDA for the business. Surprisingly, I think this is a win-win for both parties as Aramco can create some synergies ultimately increasing the fcf generation and Valvoline got to sell at a slight premium valuation. Management did also comment on a 10 year market based contract that is “advantageous for both sides.” It’s annoying they didn’t say anything more, but hopefully that implies they will get below market rates on oil. Valvoline also gets to keep the Valvoline brand for retail services globally, except for China, some South West Asian countries and North Africa. Them losing the brand for China is quite upsetting, but they only lost the Valvoline brand, not the ability to enter China or other brands they operate. Overall, I think it's a great deal for both parties, especially Valvoline shareholders who will now benefit from the ~$2.25 billion in cash for share buybacks.

The Industry

(Valvoline will now solely operate its retail services segment after the closing of the transaction, so I will not be going into Global Products)

Valvoline operates in the preventative-maintenance sector, mostly for cars and light trucks, which has both high fragmentation and a large number of tailwinds. They used to be solely an oil change service, (the industry is called quick lube) but have recently diversified into preventative-maintenance offerings. Preventative-maintenance is pretty much exactly what it sounds like, its maintenance to prevent bad things from happening to the car. That could be an oil change, refilling fluids, tire rotation, engine filter replacement, etc…

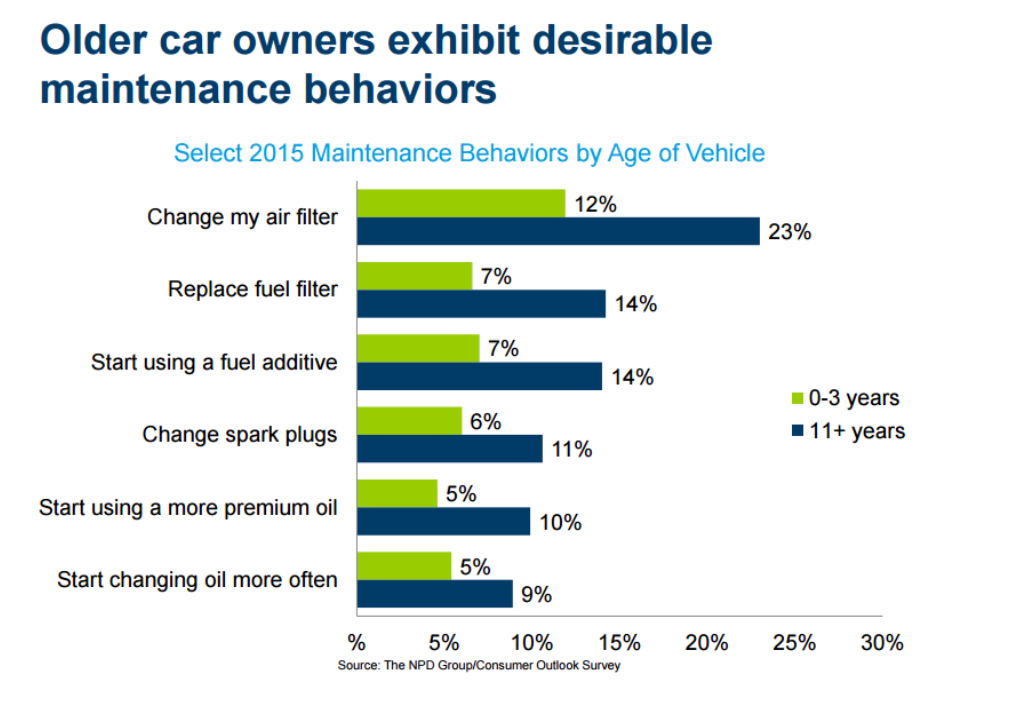

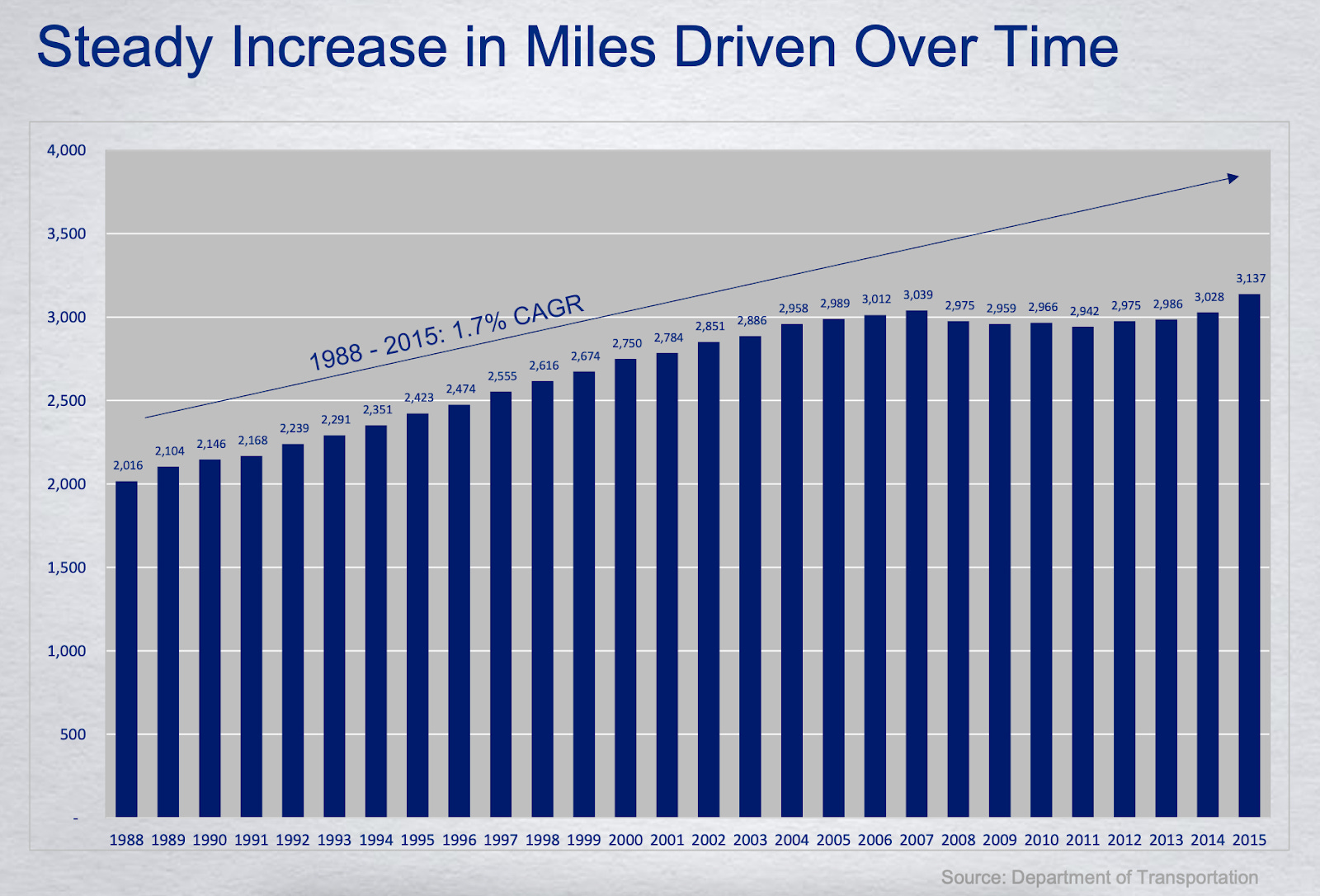

The industry is benefiting from some really nice tailwinds, mainly the increase in the average vehicle age and number of miles driven, which both increase the demand for maintenance.

As you can see, this graph is a few years old, so the 2020 predictions are off by quite a lot actually. The mean vehicle age is not 11.6 years as expected, but 12.2 years, the highest ever. Obviously the older the car, the more maintenance that is required, so that's a significant tailwind for Valvoline.

Newer cars also benefit Valvoline as well because they are often more expensive to do maintenance on. The average ticket price has increased from $77 to $90 over the last four years. Additionally, the total miles driven has increased at ~1% each year, which again causes a higher demand for maintenance.

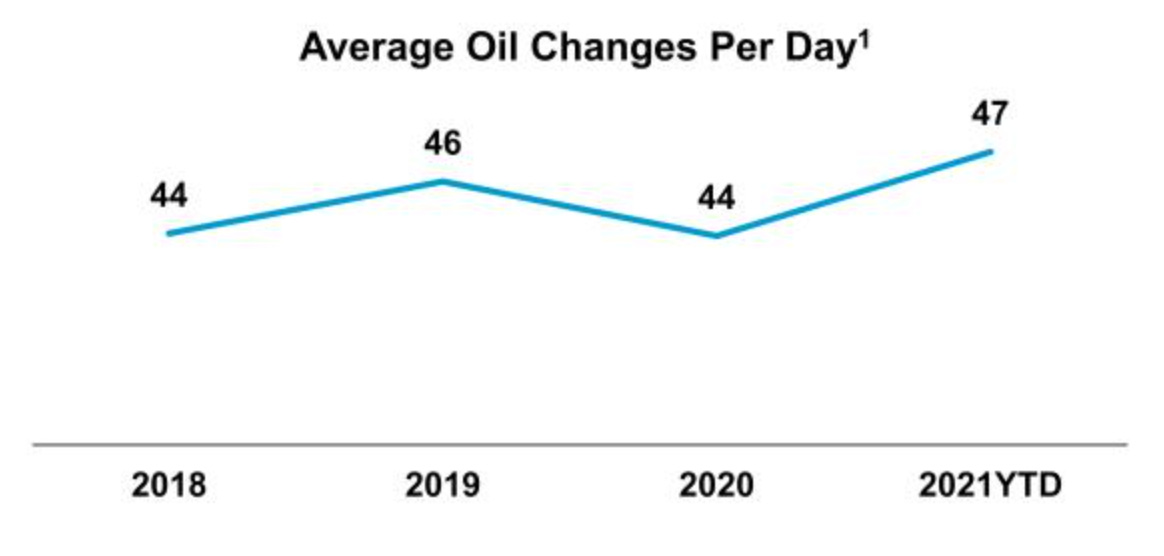

The quick change oil market is worth roughly $7 billion and expected to grow at ~0.5% annually. There are roughly 10,000 quick lube locations in the US and Canada, with 60% being non-independent and 40% being independent. These independent locations give roughly 20 oil changes per day compared to Valvoline's mid 40’s and climbing.

I would attribute the higher number of oil changes to both the Valvoline brand standing for quality, and any operating efficiencies gained through scale. Customers know what to expect with Valvoline as each employee is required to go through a rigorous training process and the brand itself has a history of innovation.

Valvoline is the second largest player in this segment, with only a 10% market share and only doing 5% of all oil changes. The preventative-maintenance market has a very long tail similar to C-stores, which allows for significant future growth through acquisitions. There was an interesting piece that I read by Fortune Financial in which they argued that highly fragmented industries, not oligopolies, are the best industries for shareholders. They lay out numerous examples as well which makes it especially interesting. I would recommend taking a quick look over the piece. Furthermore, a mechanic shortage at dealerships and tire places has caused them to shift from preventative to heavy maintenance.

Overall Valvoline benefits from scale, as well as, the larger industry tailwinds that should drive continued same store sales growth. The space is mildly competitive with companies like Jiffy Lube, but the high level of fragmentation will allow for each company to grow for a while before having to take on each other.

Unit Growth

In total, the company operates 1594 locations under the Express Care and Valvoline brands with 719 being company owned and 875 are franchised. Interestingly, Valvoline is actually buying franchises, thus more than doubling the number of company owned stores since 2017.

As a franchise model enjoyer, I’m not such a huge fan of them buying stores, but I can understand why they are choosing to buy franchised locations if the unit economics are good enough and fortunately they have got some great unit economics. After three years, company stores generate 20%+ cash on cash returns (EBITDA divided by invested capital) and at full maturity returns are north of 30%. Contrary to what has happened in the past, Valvoline mentioned on their quarterly call they will be focusing on franchises more, so perhaps we will see these trends turning around. Valvoline charges a 4% franchise fee, so that could lead to a substantial increase in margins.

The ~500 store increase since 2017 has been from roughly 50% acquisitions and 50% new openings. They tend to buy smaller operators with between 10-25 locations because in their view it decreases the time for the stores to reach maturity. Opening a store from scratch would take about 3 years to reach substantial maturity compared to an acquisition which is already at maturity. They acquired 134 service center locations for $282 million during 2021, which is 2.1x revenue per location.

Even with their almost 1600 locations, Valvoline still only reaches 15% of the US population, so there is considerable white space. The roughly 4000 independently owned and operated stores in the US and Canada should provide ample room for acquisitions to fund future growth. Valvoline expects to open between 150-160 new stores by the end of 2022, which would result in 9.5-10% unit growth year over year. This is twice as fast as competitors like Driven Brands, the owner of Meineke, and slightly faster than historic growth of ~110 stores per year. The only risk to growing faster is not being able to integrate them properly, but there really isn’t too much to do, so this growth seems both sustainable and reasonable.

Same Stores Sales

I’m extremely impressed with the same store sales growth coming from Valvoline. They have had 15 consecutive years of SSS growth. That's through both the Great Financial Crisis and COVID-19. They actually grew faster than average during 2009 and while the graph below doesn’t show it, their 2020 SSS growth was also 2.3%.

This growth during recessions undoubtedly comes from the counter cyclicality mentioned before. What's even more impressive is that the SSS growth has actually increased from an average of 4.9% to an average of 10% over the last 5 years. Of course this does include 2021 with its 21.2% SSS growth, but also COVID-19 as well and they are guiding for 12-14% SSS growth for 2022. I would assume some of this growth is coming in part from the 70% customer retention along with the average ticket price increasing at 4% annually. The industry tailwinds should allow for Valvoline to continue generating high single digit or even low double digit sales growth. That estimate is a little aggressive, so maybe mid single digits is more accurate.

Capital allocation

With so much cash coming in from the sale of Global Products, I figured this was important. Management has stated they will first pay down any debt to get to their desired leverage ratio of 2.5-3.5x net debt / EBITDA, which they are pretty much already at. Regardless, 87% of their debt is fixed rate and the first tranche isn’t due until 2030. They will also cancel the dividend and push the rest into share buybacks. That should mean they will be able to retire roughly half of the market cap with the cash from that transaction. I have no idea how aggressive they will be with the buybacks, but their last round of buybacks with much less capital averaged roughly a 2% reduction in shares outstanding. Management’s PSU’s are tied to EPS growth, so I’m fully expecting them to go balls to the walls on buybacks. I’m not such a huge fan of that because management could decide to buy back stock at insane valuations. However, on their slides they have mentioned the importance of ROIC, which has averaged high teens since IPO. That is something I like to see, but still unfortunate it's not tied to compensation.

I do like the roadmap, but compensation along with the lower inside ownership at just 0.21% does make me a little nervous. Execution could prove to be an issue in the future.

Valuation

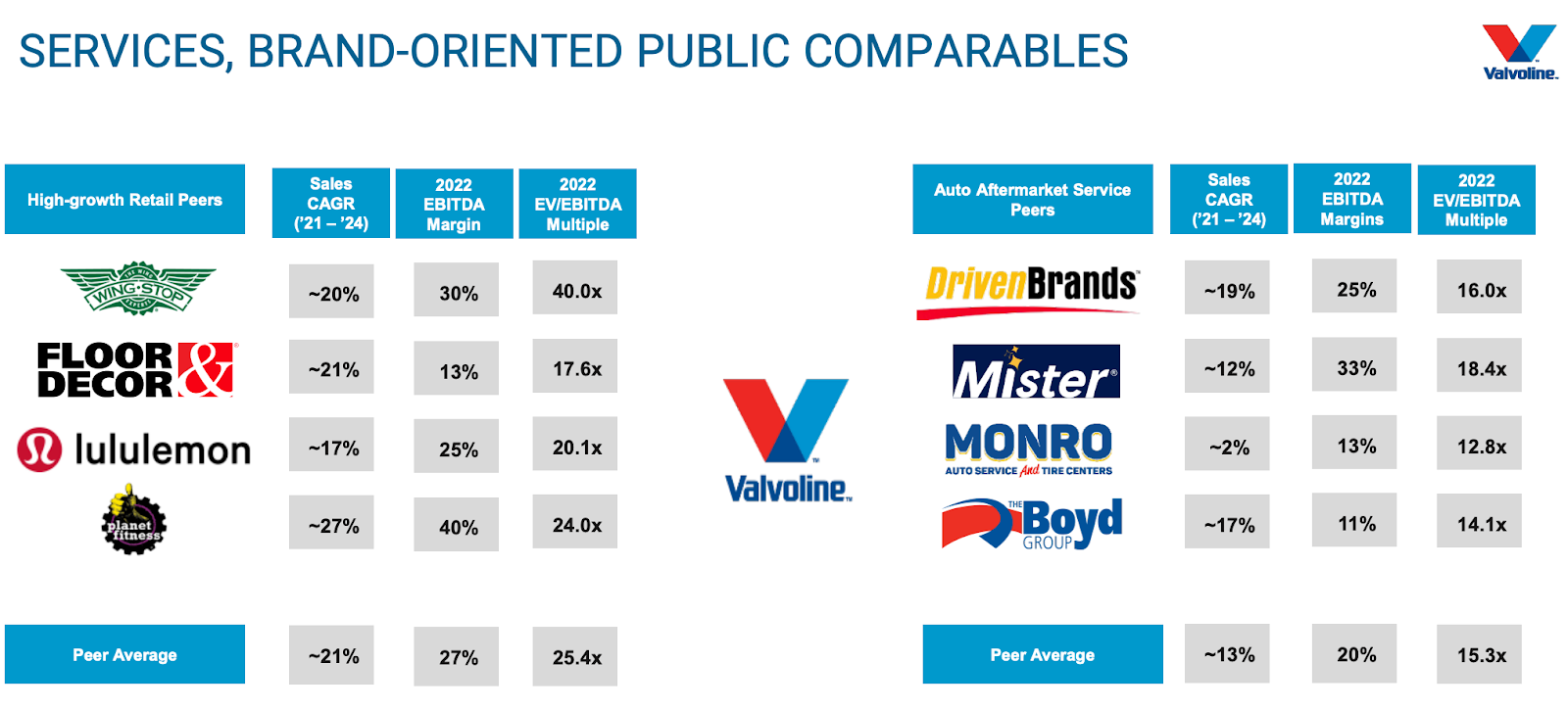

The general growth formula is the standard for many retail companies out there: SSS growth + unit growth + yield + operating leverage. For Valvoline, that equation probably fills out to 7% + 9% + 2% + 1%, or 19% growth. You will notice that the yield is only 2% and that's because I want to be conservative given that I have no idea what the actual yield will turn out to be. Management is guiding towards 20%+ EPS growth, so the buyback yield will most likely be a few basis points higher. Regardless, 19% growth is really quite nice, but the valuation also has to make sense. Looking at Valvoline’s peer group, the EV / EBITDA multiples are pretty high.

Then again maybe they aren’t with how much growth they are generating. The retail services segment generated $382 million in EBITDA last year and the EV for Valvoline will be approximately $5 billion after the sale (~$7 billion current EV - $2.2 billion from Global Products sale). That would result in a 12-13x EV / EBITDA pro forma ratio, which is slightly below the peer group.

Assuming no rerating, and only a 2% buyback yield, it looks like you could see a 19% annual return from today's price. I suspect that the buyback yield will be much higher, so maybe a low 20% 's return is more accurate. That's perfectly acceptable for me, especially for a counter cyclical business.

Potential Risks

There are a few potential risks that I could see most prominently, execution and competition. As I mentioned earlier, I am slightly concerned with the lack of appropriate shareholder alignment and low insider ownership. The CEO does have a good track record of growth, so that is slightly comforting. The business also seems fairly simple to run, so if he turns out to be an idiot I think things will be somewhat ok. Management did say at one point that they expect to be inflation resistant, but that didn’t age so well. Their excuse is such a rapid rise in product costs, which they haven’t been able to push to the consumer as quickly, and labor impacts. I’ll give them a pass as the current environment is rather crazy.

Competition will always be there, but the significant white space should stop large players from butting heads and when they eventually do I would expect mergers like what is happening with C-stores.

EV’s could pose a small risk because they don’t require oil changes or as much preventative maintenance, but internal combustion engine cars will be around for a while and Valvoline does other maintenance as well. Interestingly, they have invested in a domestic battery supply chain joint venture, but did not disclose anything else about it, and when I spoke to IR, they hinted that it will be sold along with Global Products. They were the largest supplier of battery fluid, but unfortunately this will be sold with the Global Products segment according to the IR person that I spoke to.